In corporate finance, the debt-service coverage ratio (DSCR) is the measurement of the cash flow available to pay current debt obligations. The ratio states net operating income as a multiple of debt obligations due within one year, including interest, principal, sinking-fund and lease payments.

In government finance, it is the number of export earnings needed to meet annual interest and principal payments on a country's external debts. In personal finance, it is a ratio used by funding consultants to determine income property loans.

In each case, the ratio reflects the ability to service debt given a particular level of income.

KEY TAKEAWAYS

DSCR is a measure of the cash flow available to pay current debt obligations.

DSCR can be used in analyzing firms, projects, or individual borrowers.

The minimum DSCR a lender will demand depends on macroeconomic conditions. If the economy is growing, lenders may be more forgiving of lower ratios.

DSCR Formula and Calculation

The formula for debt-service coverage ratio requires net operating income and total debt service of the entity. Net operating income is a company's revenue, minus its operating expenses, not including taxes and interest payments. It is often considered the equivalent of earnings before interest and tax (EBIT).

The Debt-Service Coverage Ratio (DSCR)

Some calculations include non-operating income in EBIT, however, which is never the case for net operating income. As a lender or investor comparing different companies' credit-worthiness – or a manager comparing different years or quarters – it is important to apply consistent criteria when calculating DSCR. As a borrower, it is important to realize that lenders may calculate DSCR in slightly different ways.

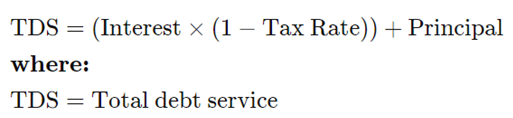

Total debt service refers to current debt obligations, meaning any interest, principal, sinking-fund and lease payments that are due in the coming year. On a balance sheet, this will include short-term debt and the current portion of long-term debt.

Income taxes complicate DSCR calculations because interest payments are tax deductible, while principal repayments are not. A more accurate way to calculate total debt service is therefore to compute:

Calculating DSCR Using Excel

To create a dynamic DSCR formula in Excel, you would not simply run an equation that divides net operating income by debt service. Rather, you would title two successive cells, such as A2 and A3, "Net Operating Income" and "Debt Service." Then, adjacent from those in B2 and B3, you would place the respective figures from the income statement.

In a separate cell, enter a formula for DSCR that uses the B2 and B3 cells rather than actual numeric values (e.g., B2 / B3).

Even for a calculation this simple, it is best to leave behind a dynamic formula that can be adjusted and recalculated automatically. One of the primary reasons to calculate DSCR is to compare it to other firms in the industry, and these comparisons are easier to run if you can simply plug in the numbers and go.

Interest Coverage Ratio vs. DSCR

The interest coverage ratio serves to measure the amount of a company's equity compared to the amount of interest it must pay on all debts for a given period. This is expressed as a ratio and is most often computed on an annual basis.

To calculate the interest coverage ratio, simply divide the earnings before interest and taxes (EBIT) for the established period by the total interest payments due for that same period. EBIT often called net operating income or operating profit is calculated by subtracting overhead and operating expenses, such as rent, cost of goods, freight, wages, and utilities, from revenue. This number reflects the amount of cash available after subtracting all expenses necessary to keep the business running.

The higher the ratio of EBIT to interest payments, the more financially stable the company. This metric only takes into account interest payments and not payments made on principal debt balances that may be required by lenders.

The debt-service coverage ratio is slightly more comprehensive. This metric assesses the ability of a company to meet its minimum principal and interest payments, including sinking fund payments, for a given period. To calculate DSCR, EBIT is divided by the total amount of principal and interest payments required for a given period to get net operating income (NOI). Because it takes into account principal payments in addition to interest, the DSCR is a slightly more robust indicator of a company's financial fitness.

In either case, a company with a ratio of less than 1 does not generate enough revenue to cover its minimum debt expenses. In terms of business management or investment, this represents a very risky prospect since even a brief period of lower-than-average income could spell disaster.

Limitations of DSCR

A limitation of the interest coverage ratio is the fact that it does not explicitly consider the ability of the firm to repay its debts. Most long-term debt issues contain provisions for amortization with dollar sums involved comparable to the interest requirement, and failure to meet the sinking fund requirement is an act of default that can force the firm into bankruptcy. A ratio that attempts to measure the repayment ability of a firm is the fixed charge coverage ratio.

Comments